Mobility and mobile apps for the enterprise space have been on my mind and on that of my team of late. In a recent blog, I looked at mobility from the customer’s perspective. Kosin Huang wrote about the benefits that mobile apps and devices bring to SMBs.

I was, therefore, very interested in Dennis Howlett’s blog yesterday, as it got me thinking about mobility from the developer’s perspective — one I hadn’t considered previously. Dennis states that apps (and, in particular, mobile enterprise apps) are here to stay and wonders about:

- The viability of a mobile (enterprise) apps market and the associated business model

- The impact that the economics of free (and paid) apps have on the development community, especially in light of the fact that many vendors are giving away their mobility apps for free.

Dennis summarizes his view: “… the notion of free mobile apps is insane” (presumably from the perspective of the individual developer.)

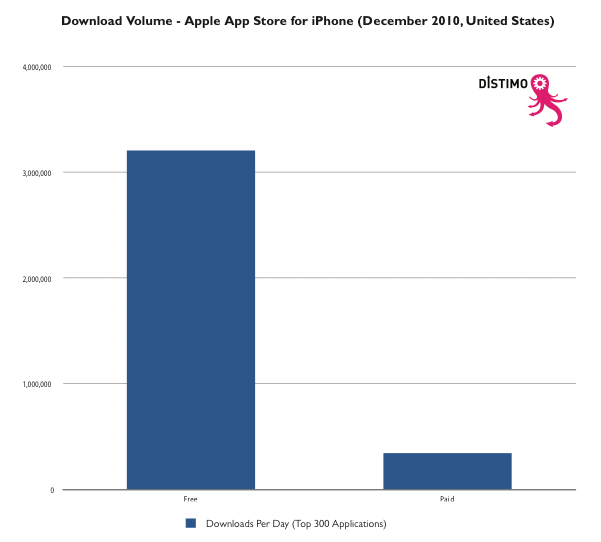

Curious, I looked around and came across an interesting report from Distimo:

No surprises – the top 300 free apps were downloaded a cumulative 3 million times/day while the paid apps were downloaded just 350,000 times/day. A perfect example of a power law. The same report states that “serious business apps” (don’t have a definition for you since I don’t have the full report) were up by 185% and grew the “strongest” while frivolous apps like angry birds grew the fastest at 802%. It is pretty clear that Dennis’ statement that mobile enterprise apps are here to stay is spot on.

The economics of the development of mobile apps are determined by:

- Who creates the app? (The vendor; an ISV; an individual developer)

- How the app is monetized? (By selling the app; By selling software related activities – like services)

- When the app is monetized? (Once, at sale; Recurring; Upon up-selling)

- The costs of placing, selling and supporting the app (Marketing; Sales; Support)

Starting with Dennis’ Q#2: Might not the answer lie in the above two paragraphs?

- The vast majority of apps will not make money – at sale. They can deliver revenue to the creator – in due course, and from related activities

- The vendors can “give away” apps; but, they are making their apps that much stickier and are driving additional sales of traditional sources of revenue – seats.

- Partners/ISVs will come out ahead, whether or not they charge for the apps. The 350,000/day downloads of paid apps are certainly contributing to the Apple exchequer. Why won’t the same dynamic hold for the partner’s coffers – many free apps and a few, but well rewarding, paid apps. Further, unlike consumer apps, there is always the services revenue that accrues from configuring the backend ERP/BI systems that collect, manage, and organize all of the company’s operational and financial data.

- Individual developers, one can argue, can roughly benefit in the same way that the ISVs do. But, based on my observation of the numbers, the number of individual developers in the enterprise space is very small. So this is, perhaps, a moot point?

Perhaps, a good way to think of free apps is in the context of a merchandizing strategy – “get 2 free, then buy 1!” The one that the customer buys more than pays for the loss leader…

Question #1 centers around the economics of an additional route to market. Instead of paying the vendor their royalty for the software that the VAR sells, the app seller is paying Apple a 30% “channel” fee. Apple, clearly, is the winner here. Does this mean that the ERP vendors will create their own app stores, just as the RIM and Android folks are doing, so they can create a “critical mass of apps” and add to their revenue stream? Will they charge a lower channel fee than Apple to attract sellers? While we wait for the answers to evolve, what is clear that there is a cost to accessing an aggregated market, any which way one cuts it.

It seems to me that there is a role for free mobile apps. And, that the paying apps will carry all the players financially while the collection of apps (paid and free) will deliver greater value to customers and mobile end users – and continue to drive greater traffic thru the apps mall. And, the toll collector will get his pound of flesh along the way.

(My thanks to Manju Bansal for hearing me out and helping clarify my thoughts!)

music")